By Julia K. Pham, CFP®, AIF®, CDFA®, Wealth Advisor featured in Kiplinger

Deciding whether to buy a house is one of the biggest financial decisions you’ll ever make. Not only is it a huge financial decision, it’s an extremely emotional one as well. Anyone who has put in an offer, experienced a bidding war and lost a house or who finally got their dream home can agree that the process can have great highs and frustrating lows.

The last few years have been increasingly confusing to potential home buyers. COVID brought on tremendous worry about the future of the economy, initially spurring home buyers to put a pause on purchases. Eventually, lockdowns and remote work and learning inspired many to seek additional space. That, coupled with a low-interest-rate environment and low inventory, spurred bidding wars and sent home prices soaring.

Now the Fed is increasing interest rates, and the housing market is cooling. There are fewer bidding wars, and we are seeing price reductions.

You may be asking yourself if now is the right time. The answer really depends on your needs and your current financial position. Here are four questions to ask yourself to see if you’re ready.

Are you ready to settle into one spot?

Buying a house is a long-term commitment, so it’s a good idea to think about whether you’re planning on making any big life changes in the near future.

If you plan on switching jobs, getting married or having kids, it might be a good idea to wait on purchasing a home, as your needs will typically change when one of these major life events occurs. If you do end up purchasing a home, you should stay long enough to offset the cost of the transaction, such as closing costs, your selling agent’s commission and expenses to prep your home for a sale. Typically, that takes about five years.

Although not the end of the world, you probably don’t want to buy a house and then find out you have to move shortly after because you landed the job of your dreams elsewhere. The best time to take on a big asset, and potentially a big liability (hello, mortgage payments!), is when you feel stable in your life and are ready to put down roots.

Have you reviewed your budget to see what you can afford?

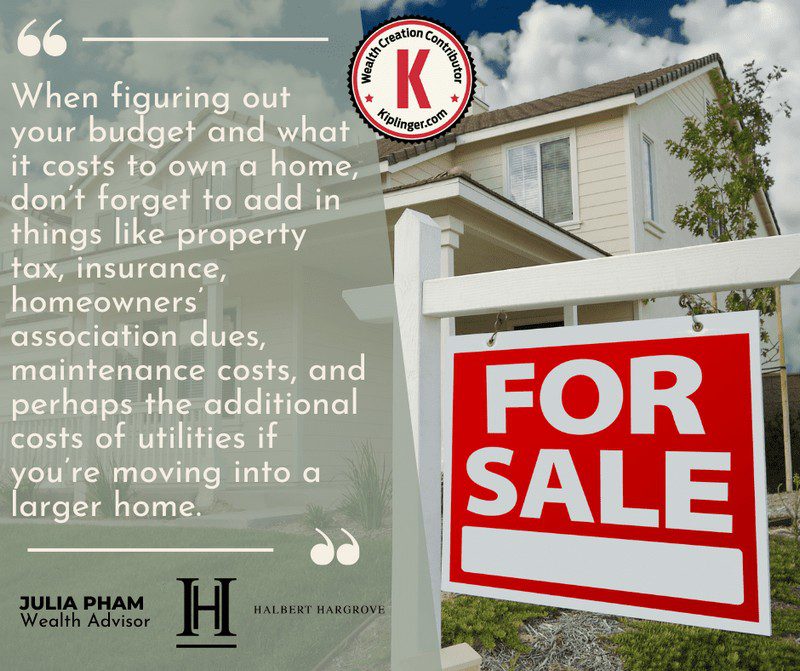

Not only are mortgages expensive, everything else that goes along with owning a home adds up. When figuring out your budget and what it costs to own a home, don’t forget to add in things like property tax, insurance, homeowners’ association dues, additional maintenance costs — think lawn care, pool upkeep, home repairs, etc.

— and perhaps the additional costs of utilities if you’re moving into a larger home. The cost of heating and cooling a large home, and water used for a garden and lawn, will obviously be more, so make sure you take those into consideration.