By: Gabrielle Olya, GoBankingRates featuring Taylor H. Sutherland, CFP®, CIMA® AIF®, Director of Portfolio Strategy/Senior Wealth Advisor at Halbert Hargrove

I am 62 years old and make about $63,000 a year. Currently, I’m putting $300 a month into my Roth IRA and $700 a month into my pension. I have $56,000 in a 401(k) and regular IRA, and an additional $6,000 in my Roth IRA. I will have a small steelworkers’ pension when I retire that will pay $200/month.

We currently owe $119,000 on our mortgage, $26,500 on a second mortgage and $9,000 on a 0% interest on a credit card (0% expires in November). We also have two car loans totaling $23,000 and we’re paying out about $550 a month on those (they have very low interest rates: 1.5% and 2.5%).

Should I switch from putting money in my Roth to paying down debt?

– Ray O’Brien

Hi Ray,

When you have battling financial priorities — in your case, paying down debt while also saving for retirement — it can be tricky to figure out how to best prioritize. To help you out, I spoke with Taylor Sutherland, CFP, director of portfolio strategy and senior wealth advisor at Halbert Hargrove. He said that figuring out where to prioritize often will depend on how you think about it — will you approach it from a left-brain, analytical perspective, or a right-brain, emotional perspective?

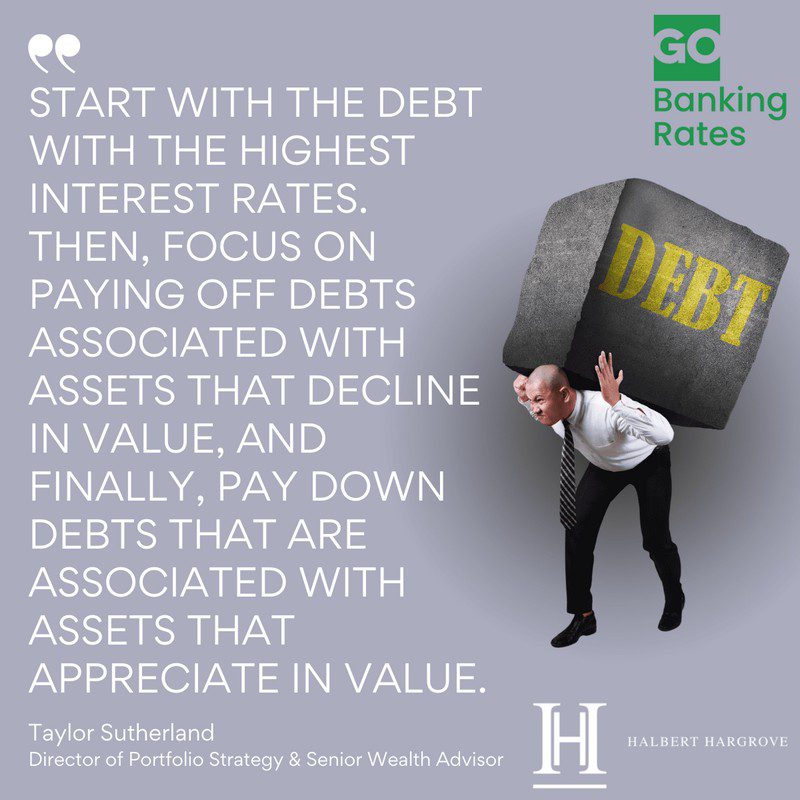

“From the left-brain perspective, you should consider retaining any debt where the interest costs are lower than your potential rate of return on the dollars you’d use to pay down those debts,” he said. “Beating the 0% rate on your credit card, and the two car loans at 1.5 to 2.5% respectively, is a no-brainer. You could put every dollar you would otherwise use to pay off those debts ($32,000) into a high-yielding FDIC-insured online cash program that is currently paying >5%. This would mean you effectively earn the difference between the 4% and the 0%, 1.5% and 2.5% rates. (I understand that you don’t have this $32,000 in hand, but every dollar you put into the Roth has the potential to out-earn the cost of those debts.)”

He notes that you may have to re-prioritize and/or make some changes once the 0% introductory rate on your credit card expires.

“You should consider either transferring to a new credit card — assuming you’ve not recently applied and your credit is sound — where they may offer another 0% preferential rate period. If that is not an option, then you should prioritize this balance over saving the additional monies into the Roth,” Sutherland said. “It is highly unlikely that you would out-earn the cost of the new higher-interest rate on your credit card debt as those interest rates are usually in the high teens, even low 20% range given currently higher interest rates. As soon as that credit card is paid off, please go back to putting money away in your [Roth].”